A closer look at the Binny Bansal ruling and what it means for NRI residency.

How it Started…

In January 2026, India’s Income Tax Appellate Tribunal (ITAT), Bangalore Bench, handed down a ruling that’s been circulating in tax circles ever since – and for good reason.

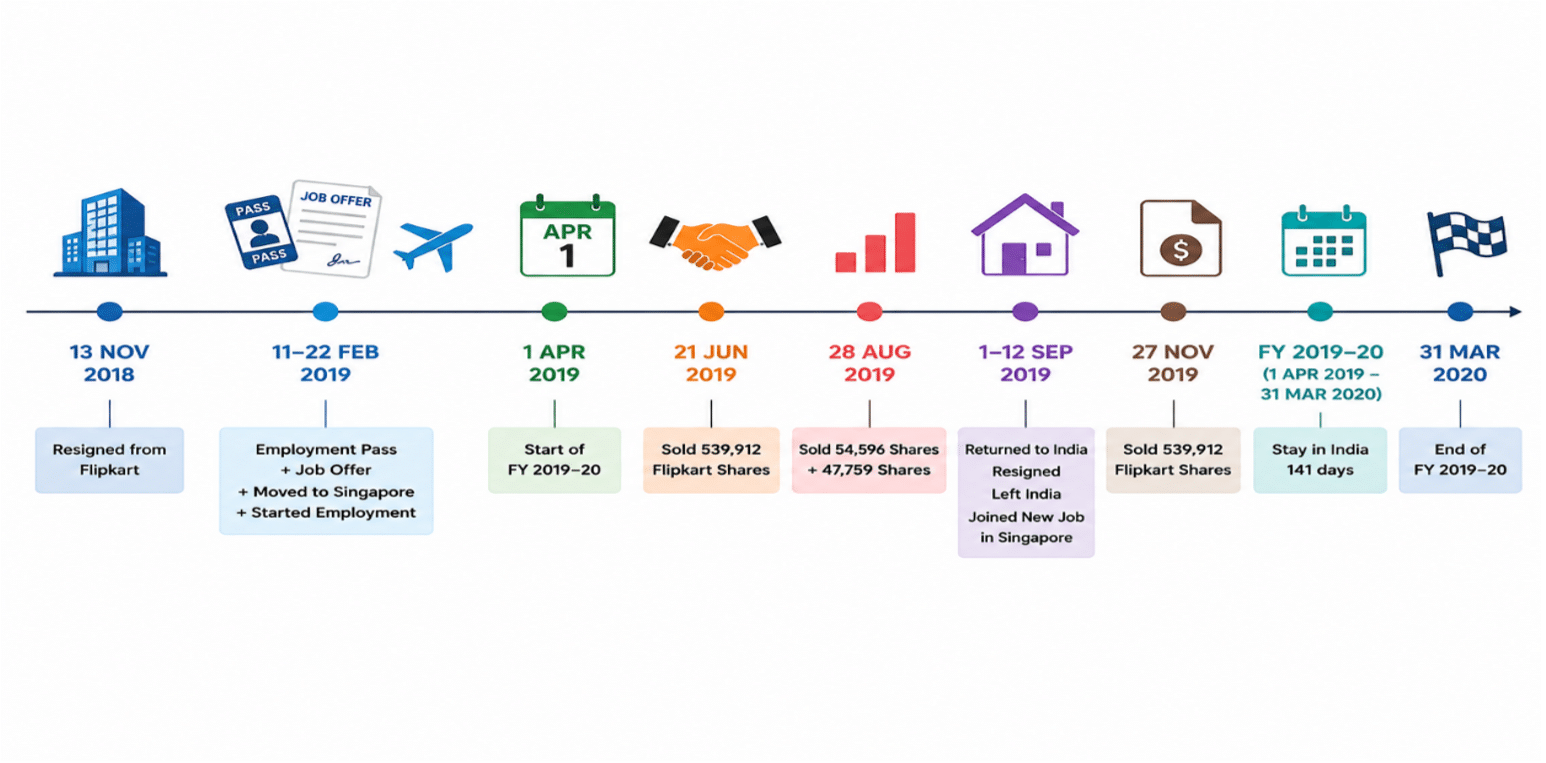

Binny Bansal, co-founder of Flipkart, had done everything you’d expect a person genuinely moving abroad to do. He’d resigned as Flipkart’s chairman and group CEO in November 2018. By February 2019, he’d secured a Singapore employment pass, taken up a job with a Singapore-based company, moved into a service apartment there, and later signed a two-year residential lease. His wife was employed in Singapore. His children were enrolled in Singapore schools. His family had Singapore permanent residency.

And yet, for Assessment Year 2020-21, the ITAT ruled he was still a tax resident of India.

| The tax department assessed his income at ₹181.94 crore for AY 2020-21 — against the ₹8.33 crore he’d originally declared as a non-resident. The gap is almost entirely explained by one capital gain of ₹162.54 crore on the sale of Flipkart shares. |

This isn’t a story about a loophole being plugged. It’s about how India’s tax authorities are now looking past passports, employment letters, and lease agreements — and asking a far harder question: where does this person’s real life actually sit?

For any founder, or NRI, this case is essential reading.

What the Tribunal Actually Looked At?

The relevant financial year is 2019-20. Here’s where it gets complicated:

1. The Day Count

- The tax department counted 141 days spent in India during the year. Bansal’s own count put it at 127 days. Either way, he was physically present in India for a substantial portion of the year — including during the early Covid-19 period.

2. The Property

- He still owned residential property in India — including a house under construction in Bengaluru’s Koramangala valued at an estimated ₹39 crore, and an apartment at Mantri Classic.

- He argued the Koramangala property was “not habitable” — still under construction. The tribunal didn’t accept that framing.

- The contradiction the bench flagged explicitly: He’d claimed a Section 54F deduction on that property — a deduction available only for buying or constructing a qualifying residential house. You can’t simultaneously tell the tax department “this is my residential property” for deduction purposes and “this isn’t a home” for residency purposes.

3. The Capital Gain

- During the year, he sold shares of Flipkart Private Limited — a Singapore-incorporated holding entity — across three tranches.

- The long-term capital gain: ₹162.54 crore.

- His position: this gain wasn’t taxable in India, either under domestic law or under Article 13(5) of the India-Singapore Double Tax Avoidance Agreement (DTAA), which generally allows residual capital gains to be taxed only in the seller’s country of residence.

Everything hinged on one question: Was he an Indian tax resident for that year, or not?

The Ruling: A Two-Step Test, and Why He Failed Both

Most people think of ‘NRI status’ as a single checkbox. The tribunal’s analysis reveals it’s actually two separate gates — and you need to clear both.

Step 1: India’s Domestic Law — Section 6(1)(c)

Under ordinary rules, spending 60 or more days in India in a year (with 365+ days in the preceding four years) makes you a resident. There’s a relaxation — Explanation 1 — that extends this to 182 days for:

- Indian citizens who leave India during that year for employment abroad (Clause a), and

- Non-residents who are merely visiting India (Clause b)

Bansal argued he qualified under one or both limbs. The tribunal disagreed on both:

- On Clause (a): He hadn’t left India during FY 2019-20 — he’d left the year before (FY 2018-19). The relaxation only applies in the year of departure, not in subsequent years.

- On Clause (b): This only applies to genuine non-residents visiting India. Bansal’s own submissions described him as someone who “resides in Singapore” and “comes on brief visits to India” — language that characterises someone visiting India, not someone outside it. It worked against him.

With no relaxation available, the ordinary 60-day rule applied. At 127-141 days in India, he was comfortably over the threshold. Result: resident of India under domestic law.

Step 2: The DTAA Tie-Breaker Test — Article 4(2)

Once you’re treated as resident in both countries under their respective domestic laws, the treaty kicks in. The DTAA’s Article 4(2) sets a four-stage sequential test. Here’s how it played out:

| Test Stage | What the Tribunal Found | |

| 1 | Permanent Home | Did he have a permanent home in both countries? Yes — long-term Singapore rental and retained Indian property. Tie unresolved. Move to next test. |

| 2 | Centre of Vital Interest | Where were his personal and economic ties closer? Family was in Singapore. But investments, shareholdings, loans to Indian entities, and the Flipkart gain were all India-rooted. RULING: India wins. |

| 3 | Habitual Abode | He had a meaningful abode in both countries, splitting time between them. In conclusive on its own — vital interest finding carried the day. |

| 4 | Nationality | Last resort tie-breaker. Indian nationality — undisputed. |

| FINAL VERDICT: Resident of India — under both domestic law and the DTAA tie-breaker test. The ₹162.54 crore capital gain remained within India’s tax net. |

Why This Ruling Has the NRI Community Worried

The unease isn’t really about the outcome. It’s about what this ruling signal for anyone who’s moved, or is planning to move, internationally. Here’s what’s genuinely troubling:

Þ ‘Centre of vital interest’ has no bright line

The tribunal itself acknowledged this is a “vexed issue” decided entirely case-by-case. You can’t build a compliance checklist around a test that’s explicitly designed to resist checklists. That’s a real planning problem for anyone trying to get this right in advance.

Þ Passive Indian investments can anchor you to India

Bansal argued his Indian holdings were legacy investments made before he ever left, and that FEMA repatriation restrictions made it impractical to move that wealth abroad quickly. The tribunal still weighed those holdings heavily against him. The implied question for any wealthy individual relocating: how much of your pre-migration Indian wealth do you actually need to liquidate or move abroad before you can credibly claim your economic centre has shifted?

Þ Property left in limbo gets read against you

Keeping a half-built house in India rather than selling it was treated as evidence of a retained permanent home — regardless of its construction status. Ambiguity about property gets resolved in favour of residency, not against it.

Þ Inconsistent positions across returns get punished

A Section 54F deduction claimed in one year resurfaced as damaging evidence in a completely separate residency dispute years later. Your past returns don’t stay in the past.

Before vs. After: What You Thought vs. What the Ruling Says

Here’s a clean breakdown of where conventional NRI planning wisdom now runs into trouble:

| Area | The Old Assumption | What the Ruling Says Now |

| Employment pass + foreign address | “I have a job and home abroad — I’m a non-resident.” | Necessary but nowhere near sufficient. Domestic day-count rules and the DTAA tie-breaker both apply independently. |

| The 182-day NRI relaxation | “As an Indian working abroad, I always get 182 days before I become resident.” | Only applies in the specific year you leave India for employment — not in later years when you’re merely visiting. |

| Retaining Indian property | “It’s under construction / not habitable, so it won’t count as a home.” | Ownership and legal availability matter more than liveability or completion. The tribunal didn’t buy it. |

| Centre of vital interest | “Once I’ve relocated, my economic centre shifts immediately.” | Assessed across the entire assessment year — pre and post-migration facts are weighed together. |

| Gains via foreign holding companies | “Routed through a Singapore entity, so it’s outside India’s tax net.” | If underlying value is Indian, the gain still feeds into the residency and taxability analysis. |

| Inconsistent filing positions | “Claims made in different years won’t be cross-referenced.” | Tribunals actively cross-check past claims (like a Section 54F deduction) against current residency arguments. |

A Note on GAAR — and Why Its Absence Here Actually Matters

India’s General Anti-Avoidance Rule (GAAR) — the broad anti-abuse provision that lets tax authorities disregard arrangements lacking commercial substance — was raised during the assessment. But it was never formally referred to the GAAR panel for invocation. The tribunal noted this explicitly and gave it no weight.

The case was decided purely on facts: Section 6(1)(c) and Article 4(2) of the DTAA. No finding of sham. No ruling that the Singapore move was tax-motivated or artificial.

| THE IMPLICATION: Authorities don’t need to allege abuse to deny non-resident status. A clean, fact-based reading of residency provisions can do the job on its own. That should worry genuine movers more than it worries tax-motivated ones — because it means good-faith relocations can still get caught if the year-by-year mechanics aren’t carefully managed. |

The 5 Principles This Ruling Cements

Strip away the celebrity’s name, and these are the durable takeaways:

- Domestic residency and DTAA residency are two separate gates. You need to clear both — winning the treaty tie-breaker doesn’t help if you’re already caught under Section 6(1)(c).

- The 182-day relaxation is a one-year window. It applies in the year you actually leave India for employment — not every year you happen to visit thereafter.

- Centre of vital interest is assessed across the full year. Move mid-year? The analysis still weighs your ties during the months you were still substantially in India.

- Ownership beats occupation for ‘permanent home’ purposes. You don’t need to be living in a property for it to count as your permanent home. Owning it and retaining the right to use it is enough.

- Indian-value assets attract scrutiny even through foreign wrappers. Flipkart Private Limited was a Singapore company. Its value came from India. That economic reality fed directly into the vital interest analysis.

The Bottom Line

The Binny Bansal ruling is really a story about timing and proof. The tribunal didn’t find that his move to Singapore was fake. It didn’t dispute that his family genuinely relocated, that he held real employment abroad, or that his life was substantively shifting.

What sank his case was that the specific assessment year in which he booked a massive capital gain fell in a transitional zone — where his Indian ties were still strong enough to anchor him to India under both domestic law and the treaty.

The lesson isn’t “don’t move abroad.” It’s far more intricate than that.

By,

Team AnBac Advisors

Disclaimer: The intent of this article is knowledge sharing with facts for increasing awareness on tax and corporate matters, and no intention exits to discuss or share opinion on any specific company or its operations.